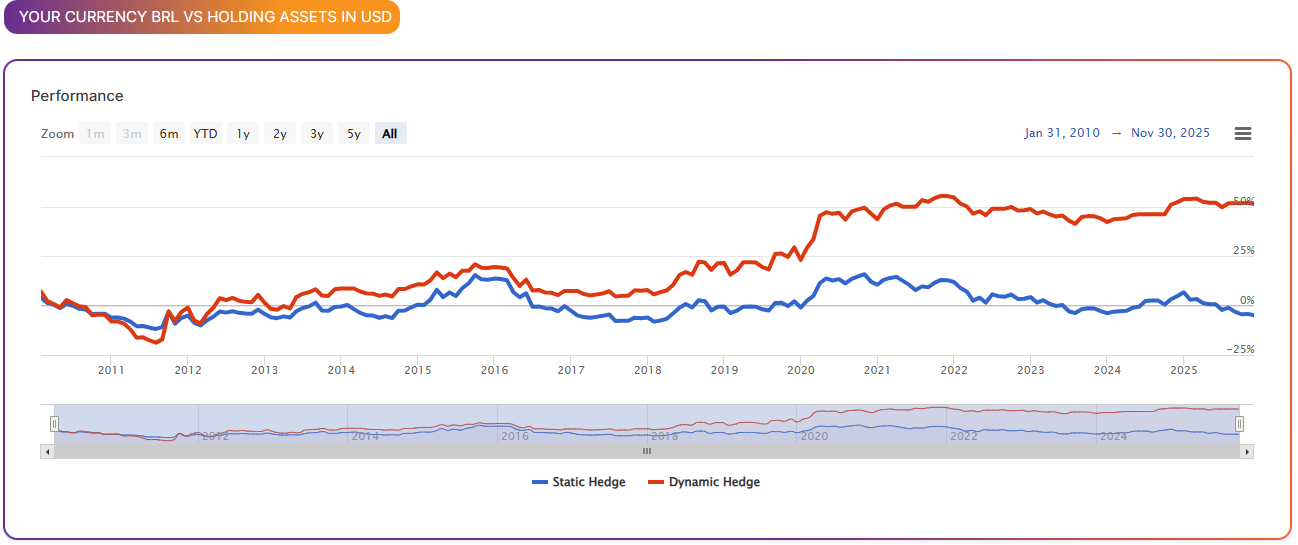

Why active hedging beats static hedging

Most companies hedge with a fixed ratio — 50% or 100% — regardless of market conditions. C8's quantitative models dynamically adjust hedge ratios based on macro-economic signals, intrinsic currency values, carry, and momentum. The result: consistent outperformance over nearly two decades of live and backtested data.

EUR/USD hedging

EUR/USD

GBP/USD hedging

track record

Head-to-head: C8 Variable Hedge vs Static Hedge

EUR/USD hedging performance, 50% benchmark, Jan 2007 – Mar 2026

| C8 Variable Hedge | Static 50% Hedge | Difference | |

|---|---|---|---|

| Annualised Return | +1.15% | −0.63% | +1.78% |

| Sharpe Ratio | 0.21 | −0.14 | +0.35 |

| Sortino Ratio | 0.29 | −0.20 | +0.49 |

| Winning Months | 57.1% | 50.6% | +6.5% |

| Realised Volatility | 5.39% | 4.55% | +0.84% |

Live model track records

C8 FX models running with real money since 2018 (Macro) and 2020 (Intrinsic) — solid line is backtest, bold purple is live performance.

What does +1.78% annual alpha mean in practice?

For a company hedging €100M in USD exposure, that's approximately €1.78M per year in improved hedging outcomes compared to a fixed 50% hedge — without changing your FX execution provider, without additional complexity, and without any integration work. Over 10 years, the compounding effect becomes substantial.

"Managing FX exposure can be complex and easy to get wrong — a combination that provides treasurers and funds with an unwelcome problem every time they buy and sell overseas assets. C8 Hedge makes the process much simpler and effective by automating the risk management process, offering users proactive strategies to optimise outcomes."

Jonathan Webb, MD, Product Manager FX

Former Global Head of FX Strategy at Jefferies · Portfolio Manager at HSBC, Credit Suisse, RBS & Bank of America · In FX markets since 1985

Jonathan Webb

Jon has been involved in FX markets since 1985 — first as an HM Treasury and City economist, then through a distinguished career as a bank and hedge fund proprietary trader. He served as MD, Global Head of FX Strategy at Jefferies, and as a portfolio manager and proprietary trader at HSBC, Credit Suisse, RBS, Bank of America, and hedge funds C-View and GLC.

Jon works alongside C8 founders Mattias Eriksson and Ebrahim Kasenally, both former partners at BlueCrest Capital Management, where they built Bluetrend into a $15B systematic fund with a significant FX component. The three originally worked together at HSBC London in the 1990s.